.png@webp)

.png@webp)

The world of cross-border payments is at a crossroads, both literally and figuratively. As the industry continues to be shaken up by new competition and technologies, this coming year will continue to show us winners and losers. The winners will be those who think beyond payment, and more about the experience around the payment, from compliance, identity management, fraud monitoring, to payment routing. The losers will be those stuck in a legacy mindset, racing to the bottom trying to make payments simpler, cheaper, and faster. In a post-pandemic world, those are table stakes.

The way we see it is there is a race emerging — between new companies and existing players – as to who can create a flywheel set of services around their core technology. While most predictions aren’t worth the paper they’re printed on, here’s a few thoughts from an industry veteran whose seen a few things:

A breakout year for A2A payments

This trend was prominent in 2023, but we’ll see it even more in 2024. Witness the reaction to FedNow’s introduction in the United States this year and multi-country linkages like Project Nexus in Asia Pacific. We agree with Forrester’s Jacob Morgan on this one. Real-time account-to-account payments will be a strong proponent in the landscape. Hundreds of more banks will launch faster payments capabilities, especially as merchants' backlash against ever-increasing card fees. We’ve seen the rise of Pay by Bank, and we will continue to see more businesses implement these options, especially in emerging markets across the world. Juniper Research agrees, saying the rise of open banking, instant payments, and merchant support will catalyze the A2A market in 2024, given these payments can be cheaper, faster and have lower risks of fraud.

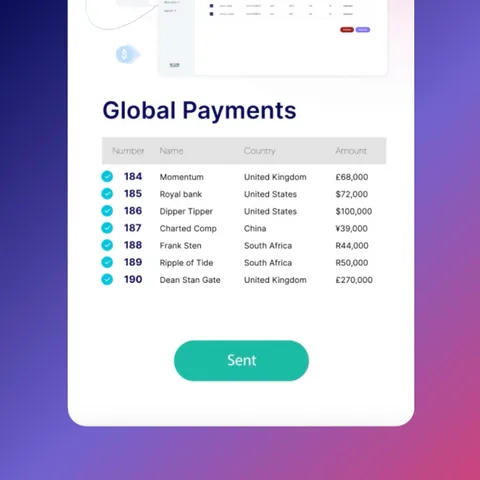

Due to this, beyond traditional bank and remittance services, innovative use cases for real-time global payments will continue to emerge in 2024. Whether its online marketplaces sending funds to their global merchant sellers, streaming platforms paying their content creators around the world, insurance companies disbursing claims across borders, or payroll platforms looking to pay employees and suppliers overseas, we’re seeing traditional and 21st-century industries embrace modern payment infrastructure. This evolution is breaking down barriers, and enabling businesses to seamlessly transact on a global scale.

AI will influence fraud in payments, but not payments in general

AI came out as the winner in 2023 with it infiltrating all aspects of tech. While we see AI having a fairly significant impact on fraud, we don’t see it changing the way payments are conducted across the world. AI tools can make fraudster attempts more sophisticated by creating activity to seem like a real person, by sending out phishing messages, or by acting as real person to gather sensitive information.

However, as digital payments become more prevalent, fraud measures are expected to become more intense. Initiatives like SEPA instant credit, a pan-European instant payment scheme that allows domestic and cross-border payments in euro to be made to and received from participating payment service providers (PSPs) anywhere in the Single Euro Payments Area (SEPA), are pushing the boundaries of real-time payments, necessitating stringent security measures. The focus on fraud prevention will drive the development and adoption of real-time payment solutions, ensuring secure and efficient cross-border transactions. However, will they be able to keep up with the quickly evolving AI innovations?

Consolidation will rise, significantly

We thought we would see more consolation of B2B payments companies in 2023, but due to the economic environment, it wasn’t as significant as we thought. Private companies are just now raising money again that will get them through the next 18 months. To show profitability, a lot of these businesses will look into M&A activity resulting in a mass consolidation of the market.

Additionally, traditional banks and payment systems will face increased competition from fintech as customers demand more seamless and tech-savvy financial services. To stay competitive, banks are increasingly collaborating with fintech players to innovate and stay strategic. Businesses are seeking alternatives to traditional banking systems, given the significant delays and hidden fees associated with international payments. Deloitte agrees that consolidation will happen, saying, “Recent events have also reiterated the importance of scale and stability. Some banks may not have the appetite to remain below certain asset thresholds. As a result, more M&A activity within the banking industry is likely.” Will collaboration continue to increase, or will consolation take the reins?

The future of payments in 2024 will be characterized by a convergence of regulatory innovation, consolidation, AI integration, and an array of real-time use cases. As the global economy becomes more interconnected, these trends will drive the development of efficient, secure, and cost-effective cross-border payment solutions, meeting the evolving demands of businesses and consumers alike.