.png@webp)

.png@webp)

.png@webp)

While some countries have begun forging relationships for businesses based outside of the networks or those looking to transfer funds to a country outside of them, the B2B cross-border payment experience remains challenging.

Although new technology has undoubtedly improved the domestic payments space, it has made the B2B cross-border payments landscape more fragmented and competitive, with fintechs, digital banks, big tech, and incumbent financial services players adopting new tools to remain relevant.

As such, many incumbents still rely on a patchwork of outdated networks, time-consuming manual processes, and inefficient networks of partners to enable payments, driving up costs, slowing the payment flow, and not providing a best-in-class customer experience.

All of this is happening at a time when global businesses are facing a transforming B2B payments landscape, driven by three key trends:

Trend 1: Global and remote workforces

Triggered by the pandemic and a raft of technological advances, it’s now commonplace for businesses to have far more international workforces. According to a Nium survey, between 2020 and 2021, the share of firms that expanded their hiring of international workers grew nearly six times, from 8% to 46%. Not only are these employees overseas, but they’re also remote. In 2019, just 17% of global employees1 worked remotely. Today, 32% are now entirely remote, with 51% working in a hybrid work/home environment.

Furthermore, they often consist of full-time staff as well as domestic and, increasingly, overseas freelancers. Sixty-eight percent of companies in the U.S. have outsourced their services2 to low-cost countries.

This poses a number of payment challenges.

Complex expenses

- The growing size and variety of expenses mean employees need to be reimbursed immediately. Despite this, one-third of staff3 still wait over a month for expense reimbursement. Not only is this unfair to the employee, but it puts the business at risk of losing them, with 76% of financially stressed4 employees admitting to being attracted to other companies.

Costly exchanges

- The cost of paying workers in their local currency can vary significantly due to fluctuating FX rates, bank charges, and transaction fees depending on the payroll service provider or rails involved.

Need for faster payments

- When working with emerging markets, the speed of payment is a key capability. In Malaysia5, for example, 55% of on-demand workers have less than three months’ financial buffer. Meanwhile, in India6, 88% of the on-demand workforce runs out of money before the month is even out.

Contrasting payment methods

- Nearly two billion adults globally7—one-third of the world's adult population—remain unbanked, with almost all living in emerging markets. In response to the lack of traditional infrastructure, more people in these regions turn to alternative forms of payment, with the share of adults making or receiving digital payments in developing economies growing from 35% in 2014 to 57% in 20218, outpacing growth in account ownership.

Trend 2: Global Businesses

The corporate world is now a global playing field, with the ability to expand overseas vital to stay competitive. Forty-nine percent of U.S. companies surveyed in 20219 said their best opportunities are outside of their home region, compared to 35% in June 2020. Meanwhile, an HSBC poll of mid-market enterprises across 14 different markets in late 2022 found that two-thirds10 planned to expand internationally in the next 12 months.

This, too, poses new challenges.

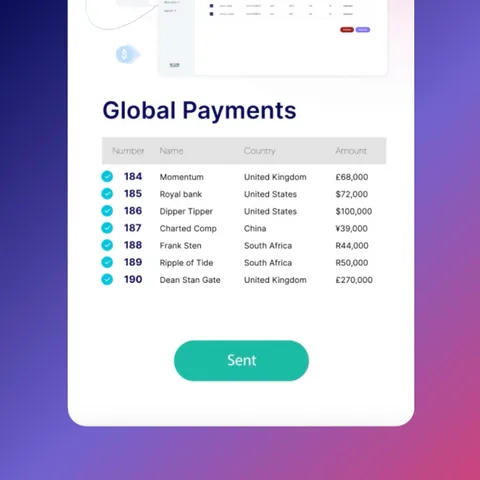

Increase in B2B cross-border payments

- Fifty-eight percent of SMEs11 say they are sending and receiving more B2B cross-border payments now than before the pandemic – a significant increase from 2020, when 38% surveyed said they had increased their use of B2B cross-border payments since the pandemic began. Despite this, U.S. businesses still wait an average of 33 days to receive payments12 from their cross-border business partners, while U.K. businesses wait an average of 30 days.

Compliance and security concerns

- To transfer money and operate overseas without the use of a B2B payments provider, global businesses must forge new banking relationships and gain access to local rails, all while making sure they’re compliant with local regulations. Doing this is costly and time-consuming. This also raises concerns around security, with nearly 55% of businesses13 saying they worry about fraud and data security when receiving international payments.

Trend 3: End-users now expect more

Thirty-nine percent of SMEs14 now say that ‘cross-border payments slow down our supply chain’ while 36% say there’s ‘no transparency about how much money we lose in foreign exchange’.

For modern businesses and consumers, this just isn’t acceptable. They expect B2B cross-border payments to be as fast and intuitive as other areas of their digital lives. The growth of e-commerce, alternative payments methods, and mobile payments have created a need for faster, cheaper, and more transparent B2B cross-border payment solutions, but existing systems are falling behind.

As a result, 72% of SMEs14 are using web-based payment platforms from banks, money transfer companies, and other providers, and approximately two-thirds are using mobile apps.

Real-time cross-border payments, along with the right B2B payments partner, offer a solution to these problems.

Final Thoughts

.png@webp)

To deliver a truly localized payment solution, it should encompass real-time transactions in various currencies utilizing both local and international payment networks. Additionally, it must adhere to local regulations and provide access to competitive foreign exchange rates.

While achieving this independently may be challenging for many, it is crucial to identify the right B2B payments partner, such as Nium, that possesses the necessary infrastructure, payment networks, and established relationships to meet the demands of modern global enterprises.

Connect with one of our payment experts today to find out how Nium can aid your business or financial institution in accessing the world’s real-time payment networks.

1 https://nordlayer.com/blog/welcome-to-global-remote-work-index/

2 https://www.outsourceaccelerator.com/articles/outsourcing-statistics/

3 https://www.unleash.ai/hr-technology/1-3-of-staff-wait-over-a-month-for-reimbursement/

5 https://www.paulhypepage.my/gig-economy-in-malaysia-pros-cons-and-regulations/

8 https://www.worldbank.org/en/publication/globalfindex

11 https://b2b.mastercard.com/media/sgperrmp/borderless-payments-report-2022.pdf

14 https://b2b.mastercard.com/media/sgperrmp/borderless-payments-report-2022.pdf