Stablecoins are rapidly evolving from niche infrastructure into a foundational layer of global payments.

But while the use cases are becoming clearer, the ecosystem behind them remains complex. Who actually does what? Where does risk sit? And how does value move from one party to another?

This piece breaks down the stablecoin ecosystem in plain terms, outlining the key layers, the players in each, and how it all fits together.

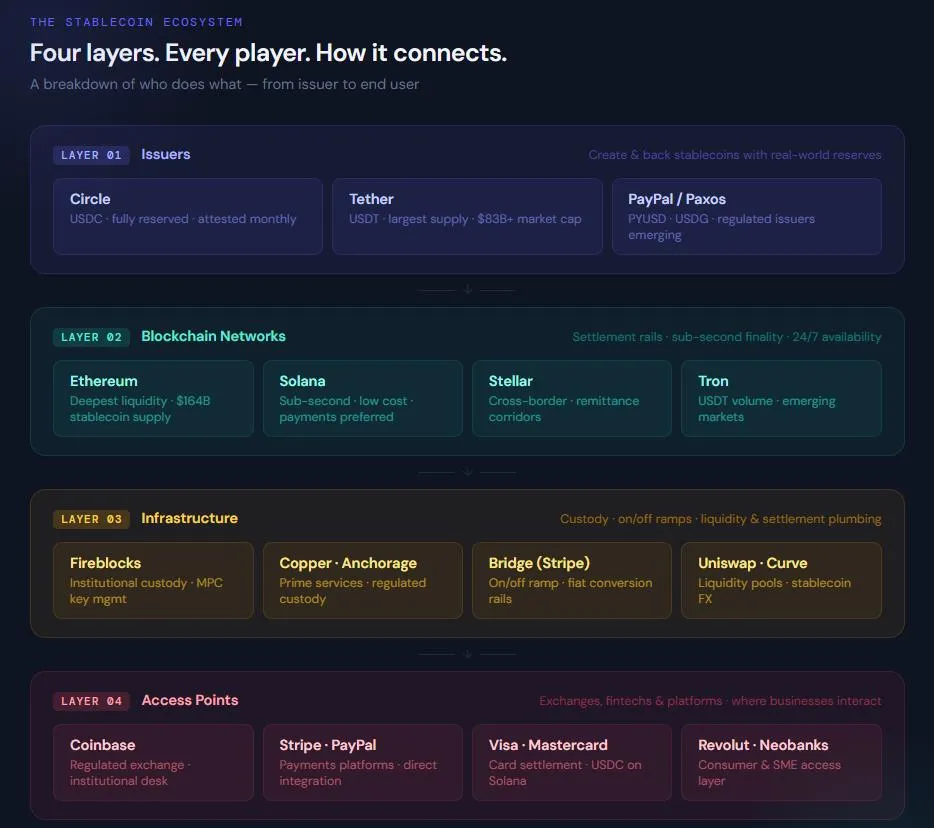

Think of it as four layers

The simplest way to understand the stablecoin ecosystem is to break it into four distinct layers, each with its own role and set of players.

Layer 1: The Issuers

These are the companies that create stablecoins and back them with real-world assets, typically cash and short-dated government securities held in segregated reserve accounts.

Circle (USDC) and Tether (USDT) are the dominant players.

When a bank transfers $10m to Circle, Circle mints $10m of USDC. When that USDC is redeemed, Circle burns it and returns the dollars.

The issuer is essentially running a narrow bank. The credibility of the stablecoin is only as strong as:

- the quality of its reserves

- the transparency of its attestations

- the trust in the issuer itself

Treasury takeaway

Treat stablecoin issuer due diligence the same way you would a bank counterparty review. Understand reserve composition, attestation frequency, and issuer credibility.

Layer 2: The Networks

Stablecoins do not move through SWIFT. They move across blockchain networks, which are distributed ledgers that record and settle transactions.

- Ethereum is the longest-established network with the deepest liquidity

- Solana is increasingly favoured for payments because of speed and low cost

- Stellar is purpose-built for cross-border payments

- Tron carries a significant share of USDT volume, particularly in emerging markets

For treasurers, the key questions are:

- settlement finality

- transaction costs

- network reliability

- and critically, which networks counterparties and liquidity providers support

Layer 3: The Infrastructure

This is the layer most people do not see, but it is where the operational plumbing sits.

Custody and wallet infrastructure

Players like Fireblocks, Copper, and Anchorage act as institutional-grade wallet providers. They handle key management, transaction signing, governance, and auditability.

For regulated fintechs, this is non-negotiable.

On and off ramps

Providers such as Bridge (Stripe), MoonPay, and Banxa handle conversion between stablecoins and fiat. This is a critical step in making stablecoins usable in real-world payments - an area where platforms like Nium are helping extend that utility into everyday spend.

This is where:

- on-chain meets banking rails

- liquidity and pricing matter

- counterparty risk becomes real

Settlement and liquidity layer

Protocols and market makers provide routing and liquidity between stablecoins and networks.

Think of these as the FX desks of the on-chain world.

Layer 4: The Access Points

This is how institutions and users actually interact with the ecosystem.

Centralized exchanges

Coinbase, Kraken, and Binance provide access to buy, sell, and hold stablecoins.

For treasury teams, the focus should be on:

- custody standards

- reporting

- compliance

Fintech and payments platforms

Stripe, PayPal, Revolut and others are increasingly embedding stablecoin capabilities directly into their products.

This is the layer that will bring stablecoin rails into mainstream business payments without requiring every company to manage wallets directly.

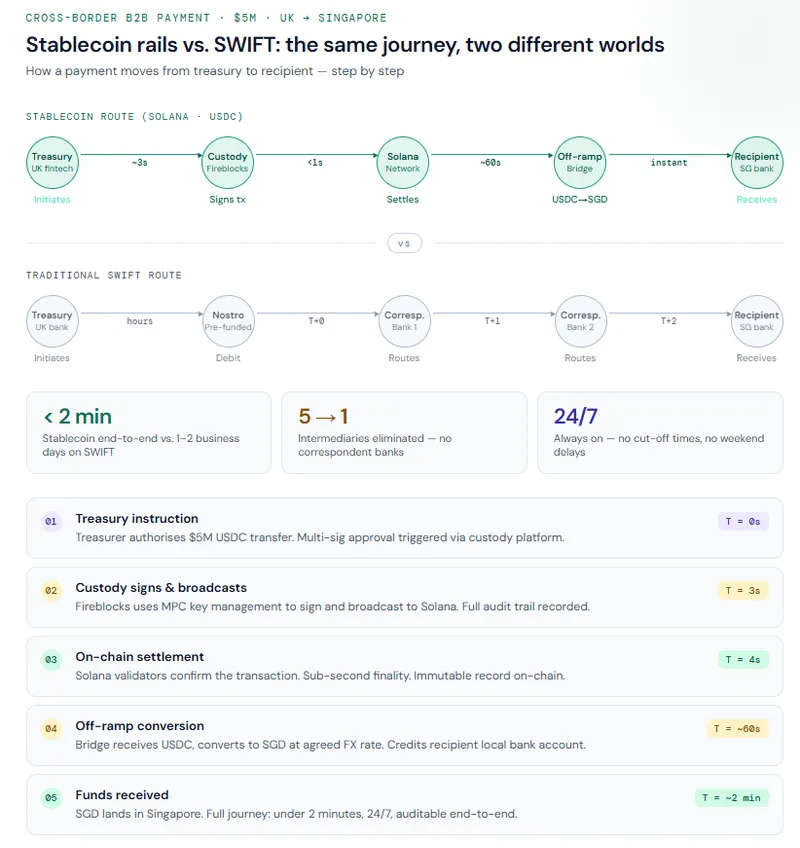

How a Stablecoin payment actually flows

Put it all together, and a cross-border B2B payment looks like this:

- A treasurer instructs their custody provider (Layer 3) to transfer USDC

- The transaction settles on a network such as Solana (Layer 2) in seconds

- The recipient converts USDC to local fiat via an on or off ramp (Layer 3)

Result:

- settlement in minutes, not days (validated by the Federal Reserve analysis on stablecoins and cross-border payments)

- significantly reduced pre-funding requirements

| Traditional SWIFT | Stablecoin Rails | |

| Settlement time | 1–2 business days | Under 2 minutes |

| Pre-funding | Nostro accounts required | Minimal |

| Intermediaries | Up to 5 correspondent banks | None |

| Availability | Business hours, weekdays | 24/7 |

| Cost | High — fees at each intermediary | Significantly lower |

| Transparency | Limited visibility mid-transfer | Full audit trail on-chain |

The ecosystem is still maturing

A few realities are worth calling out:

- Not all layers have the same depth of institutional infrastructure

- On and off ramp liquidity varies by corridor

- Regulatory clarity differs across jurisdictions

- Cross-chain interoperability still introduces risk

None of these are blockers.

However, they are things a disciplined treasury team should map before deployment, not after.

Who wins next?

The fintechs that understand this ecosystem now, including who does what, where risk sits, and which players are truly institutional-grade, will be best positioned to deploy it with confidence.

Exploring stablecoins as part of your payments or treasury strategy? Discover how Nium is enabling businesses to unlock real-world utility from stablecoin balances.